The Best Banks for Startups in 2026: The Honest, Updated Guide

Last updated May 18, 2026

Startups have banking needs that are more nuanced than the regular banking system. So, we've created a list of the best banks for startups in 2026.

It has been long enough since the Silicon Valley Bank collapse that most founders have moved on. The lesson, unfortunately, is the part most people moved on from too.

The original version of this article ranked Chase at number one and treated big banks and startup-native platforms as if they belonged on the same list. That framing was wrong, and we are fixing it. A tech founder who banks like a dental practice is taking on risk they cannot see, and the SVB failure is what that risk looks like when it arrives.

This is the rebuilt 2026 guide. It is organized the way founders actually bank now: a primary platform, a card and spend layer, and a treasury or sweep layer for the cash that matters. We will tell you which providers fit which job, where each one is weak, and what changed in the last year, including one acquisition that quietly merged two of the entries from the old version of this list.

The one concept that should drive every banking decision: FDIC coverage

Standard FDIC insurance covers $250,000 per depositor, per bank. That is the entire SVB lesson in one sentence. The founders who got hurt were not reckless. They simply had a seed or Series A round sitting in a single checking account, far above $250,000, at a bank that failed over a weekend.

In 2026 the question is no longer "which bank has the nicest app." It is "how do I hold several million dollars of raised capital with real deposit protection without juggling four logins." Modern startup banking platforms answer this with sweep networks: software that spreads your balance across many partner banks, each insured to $250,000, so total coverage scales into the millions. Treasury products solve the same problem a different way, by moving idle cash into government money market funds or short-dated Treasuries, which are not FDIC insured but carry a comparable risk profile and usually a higher yield.

Every recommendation below is filtered through this lens. After a Series A, you will exceed the $250,000 cap immediately, so the right answer is almost always a platform with an extended sweep, plus a separate treasury bucket for the cash you are not spending in the next quarter.

The modern startup banking stack

Before the list, here is the mental model. Most well-run venture-backed companies in 2026 do not use one bank. They use a stack:

The primary account is where operating cash lives and where payroll and vendors are paid. This is your Mercury, Rho, or for some, a traditional bank. The spend layer is corporate cards plus expense and approval controls, often Brex or Ramp, though Rho and Mercury now bundle this. The treasury layer is where post-raise cash earns yield while staying protected, through Mercury Treasury, Rho, Meow, or a high-sweep bank like Grasshopper. And the optional credit layer is venture debt or a line of credit, which is where SVB under First Citizens still leads.

The list below is grouped by what each provider is actually for, not ranked one through ten as if they were interchangeable. They are not.

Tier 1: Startup-native platforms (where most founders should start)

These are built for venture-backed and high-growth companies. They are the core of the modern stack.

Mercury

Mercury is one of the two default primary accounts for first-time founders, especially out of accelerators. Free checking and savings with zero minimums, a clean interface, and up to roughly $5 million in FDIC coverage through partner-bank sweep networks. Treasury by Mercury moves idle cash into government-backed money market funds managed by partners including J.P. Morgan and Morgan Stanley, currently yielding in the mid-3% range, and the IO credit card offers 1.5% cashback with no personal guarantee.

One important 2026 update: Mercury applied for its own national bank charter in December 2025 and received conditional OCC approval to establish Mercury Bank in April 2026. Final FDIC and Federal Reserve authorization is still pending with no confirmed timeline, so for now Mercury remains a fintech operating through partner banks, not a chartered bank itself.

Best for: pre-seed through Series A founders who want simplicity and clean FDIC coverage and do not yet need integrated bill pay or phone support.

From our practice: Full disclosure, we use Mercury at the firm and have for years. We have no business relationship with them, no referral deal, and no affiliate link anywhere on this page. We just think it works. Across the founder clients we run finance operations for, it is consistently the account that causes the fewest problems: fast to open, clean to reconcile, and the sweep coverage means we are not engineering FDIC workarounds for early-stage clients. It is the default we set up first for most new clients, which is exactly why it earns the disclosure here rather than a footnote.

Watch for: no cash deposits, support is primarily chat and email with phone access gated to higher tiers, the full feature set is paywalled on plans that reach into the hundreds per month, and Treasury is an investment product covered by SIPC, not FDIC. Note also that Mercury's partner-bank arrangements have drawn regulatory attention in the banking-as-a-service space, which is worth understanding rather than ignoring.

Rho

Rho is the strongest fit once a company is consolidating its finance operations rather than just opening a bank account. It bundles banking, corporate cards, bill pay, expense management, and treasury into one platform with no platform fee, and its extended FDIC coverage runs far higher than Mercury's through its partner-bank arrangement. It is increasingly the default at the Series A and later AI-heavy tier specifically because the controller is not stitching four tools together.

Best for: Series A and later companies that want one integrated finance platform from day one through scale, and teams that value AP automation and native ERP sync.

Watch for: a meaningful minimum balance to open, which prices out the earliest-stage startups, no physical branches, and no traditional lending products.

Brex (now a Capital One company)

This is the entry that changed the most, and the reason the old article needed a rebuild rather than a refresh. Brex and Capital One are no longer two separate options. Capital One announced the acquisition of Brex in January 2026 and completed it in April 2026 in a deal valued at $5.15 billion. Brex now operates as part of Capital One, which is using it to move beyond commodity cards and deposits toward owning the center of a CFO's operating stack.

The product itself continues to operate and remains one of the strongest spend-management platforms: corporate cards with no personal guarantee, AI-driven expense automation, multi-currency operations across many countries, travel management, and treasury with high FDIC coverage. The combination with Capital One's balance sheet and underwriting is, on paper, a serious advantage. The open question for founders is integration risk: how the product, pricing, and famously startup-friendly eligibility evolve now that it sits inside a top-tier consumer bank rather than running as an independent fintech.

Best for: venture-backed companies focused on spend management and global operations, particularly those with distributed international teams.

Watch for: eligibility has always effectively required venture funding or strong revenue, which excludes bootstrapped startups, premium tiers carry per-user pricing, and the Capital One integration is new enough that its long-term effect on the product is genuinely unknown. This is a "watch the next 12 months" situation, not a reason to avoid it, but founders should know it is no longer an independent company.

Bluevine

Bluevine is the value pick for operating cash. It pays a competitive APY on checking balances, well above what any traditional bank pays on idle operating money, with no monthly fees on the standard account and insured cash sweep coverage. It also offers a genuine line of credit, which most pure startup-native platforms do not.

Best for: capital-efficient and bootstrapped startups that want real yield on operating cash and an actual lending product without venture backing.

Watch for: no physical branches or cash deposits, the top APY tiers require qualifying activity or a paid plan, and it is more of a banking product than a full finance operating system.

Tier 2: The treasury and high-coverage layer

Once a round lands, the operating account is not where most of the cash should sit. This tier is about protection and yield on the balance you are not spending soon.

Grasshopper

Grasshopper is the under-the-radar pick for high deposit protection on a chartered bank. It is a fully digital, OCC-chartered national bank focused on the innovation economy, with extended FDIC coverage well into the eight figures through its sweep network, business checking that pays a competitive APY on operating balances, and an SBA lending program that startup-native platforms do not match. The distinction worth knowing: it is a chartered bank, not a fintech on top of a partner bank, which materially simplifies the regulatory picture for clients.

Best for: funded startups holding significant post-raise cash that want a startup-native chartered bank and the highest deposit protection on this list.

Watch for: it is primarily a banking and treasury product, not a full spend-management stack, so most companies use it alongside a cards and expense tool. It is also a smaller institution by total assets than the partner banks behind some fintech platforms.

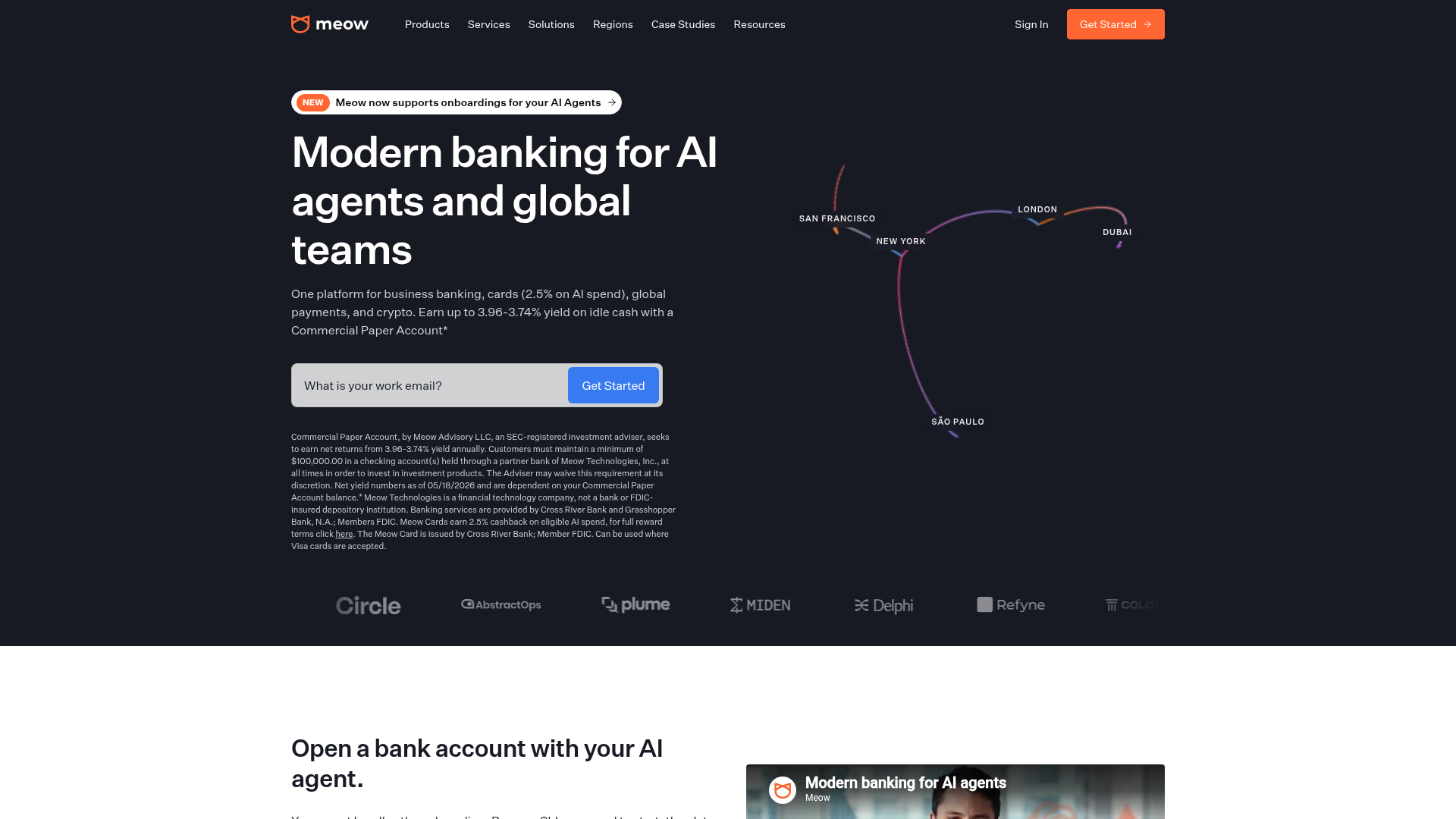

Meow and Mercury Treasury

For pure yield on excess cash, Meow runs a treasury-focused platform that puts cash into money market funds and Treasury bills held in custody, with very high effective coverage through its partner network, aimed at startups comfortable directing their own cash strategy. Mercury Treasury is the simpler in-house equivalent for companies already on Mercury. Neither is a primary operating account. They are the yield layer that sits behind one.

Best for: cash-heavy companies post-raise that want Treasury-level yield and either want to self-direct (Meow) or keep it simple inside an existing platform (Mercury Treasury).

Watch for: Meow is a younger, smaller company than the Tier 1 platforms, and treasury products are investment vehicles, not FDIC-insured deposit accounts. Understand the risk profile before moving the bulk of a round.

Tier 3: The credit layer for venture-backed scale-ups

Silicon Valley Bank (now part of First Citizens Bank)

Yes, this is the bank from the 2023 collapse. It was acquired by First Citizens the same month it failed, and it still owns one specific lane: venture debt and growth capital for venture-backed companies, plus deep VC network access and specialized technology and life sciences teams.

The honest framing in 2026 is narrow. Newly incorporated startups are largely not choosing SVB as a primary bank post-collapse, and that is rational. But for a Series A and later company that specifically needs venture debt or SVB's investor network, it remains a credible option, almost always as a credit relationship layered on top of a startup-native primary account, not as the only place the cash sits.

Best for: Series A and later venture-backed companies that need venture debt or the VC network specifically.

Watch for: standard $250,000 FDIC coverage rather than an extended sweep, premium pricing relative to digital platforms, a relationship-banking model that is heavier than an early-stage founder needs, and ongoing uncertainty about product direction under First Citizens. Do not concentrate an entire round here.

When a traditional bank actually makes sense

The old article ranked Chase and Bank of America as top startup banks. For a venture-backed tech startup, that is the wrong default. These institutions pay almost nothing on cash, cap FDIC at the standard $250,000 unless you actively opt into a sweep, and are built for general small business rather than the innovation economy.

That said, there are real, specific reasons a startup adds a traditional bank, and honesty requires naming them. You need to deposit physical cash. You want an SBA loan, which the startup-native platforms generally do not offer. You want a national branch network for in-person service. Or you are at a stage and scale where a dedicated commercial relationship genuinely adds value.

If those apply, Chase and US Bank are the most defensible choices, primarily for their SBA lending and branch access, and almost always as a secondary account beside a startup-native primary, never as the place a seed round sits earning 0.01%. This is a deliberate, scoped role, not the top of the list.

How to actually choose: the 2026 default

There is no single best bank, and any article that gives you one is selling something. The honest default for most venture-backed startups in 2026 looks like this. A startup-native primary account, Mercury early or Rho as finance operations get complex. A spend layer, Brex or Ramp, recognizing Brex is now a Capital One company. A treasury layer for post-raise cash, Mercury Treasury, Rho, Meow, or Grasshopper for maximum coverage. And, only if needed, a credit layer through SVB under First Citizens for venture debt.

The single worst choice in 2026 is the 2021 playbook: an entire round in one checking account, no treasury product, no sweep, no secondary bucket. That is the exact decision the SVB collapse should have ended, and it is still the most common mistake we see.

Where this gets decided in practice

Banking setup is not a one-time form. It is FDIC coverage analysis, treasury deployment, the right primary and secondary split, and a structure that survives the next raise. It is also exactly the kind of decision that quietly compounds on your cap table months later if it is done casually.

This is part of what a fractional CFO actually handles. If you want a banking and treasury structure designed around your stage and runway rather than copied from a list, that is a conversation worth having before the next tranche lands, not after.

This guide is updated as the market changes. Banking products, FDIC coverage limits, yields, and ownership all move, and this article reflects the landscape as of mid-2026. Verify current terms on each provider's site before opening an account, and treat any single number here as directional rather than a quote.