Debt financing methods, such as small business loans, are common in late stage startups. There are two main ways to acquire money in order to quickly expand your startup business assets called debt financing and equity financing.

You might already be familiar with these terms but through this article, we shall explore each one in more detail, and determine why late-stage startups tend to prefer debt financing, over equity financing.

What Is Debt Financing?

Debt financing occurs when you sell debt instruments, such as bonds, notes, or bills, for instant financial leverage with the intention of repaying the amount borrowed with interest by a predetermined date.

The main thing to note is that debt financing involves fixed income products, meaning any product that has a set value so you know precisely how much you’re borrowing and what is needed for repayment.

How Debt Financing Works

The three main types of debt financing are installment loans, revolving loans, and cash flow loans. There are also two sub-terms called short term debt financing and long term debt financing.

Let’s take a closer look at each of them:

Installment Loan

The installment loan is perhaps the most traditional type of debt financing involving a basic upfront lender to whom you will repay the loan with fixed interest payments over a scheduled time period.

Installment loans can be secured or unsecured. A secured loan requires that you have some form of collateral, such as a car or house, that can be used in the event you are unable to repay your debt. You will be able to borrow more on a secured loan than on an unsecured loan.

Revolving Loan

A revolving loan works like a credit card where you have a certain line of credit that you can spend up to. Any credit that you’ve spent will slowly gain interest if not paid off. You can choose to use and pay off as much as you want at any time.

The revolving loan is quite useful when you just need a few extra things that are out of your budget. You can then pay them back as your sales start coming in.

Cash Flow Loan

Cash flow refers to your startup’s typical earnings over a period of time. A potential lender will look at your accounts to determine the size of the loan that you would easily manage to repay, based on those findings. A couple of examples of cash flow loans are merchant cash advances and invoice factoring.

Unlike installment loans, cash flow loans are determined by a different repayment model. Typically, repeat payments are made bi-weekly or monthly and usually come with early repayment fees.

Short Term Debt Financing

Short-term debt financing involves a loan term of up to 12 months. You will typically opt for a short-term loan when you’re seeking a small business loan to push your late-stage startup over the finish line and transform it into a fully-fledged business.

The monthly payments will be considerably higher with a short-term plan, so make sure you can keep up with them.

Long Term Debt Financing

Long-term debt financing involves a loan term of 12 months or longer. We generally refer to a loan as long-term when it extends from 10 to 25 years. You will opt for a long-term loan for a significant pivot, such as a site overhaul, or for acquiring an existing company.

Types Of Debt Financing

We’re going to look at six of the more common types of debt financing. It is quite likely that one of these options will suit your needs, but make sure you look at further options if they aren’t 100% to your liking.

Business Term Loans

Business term loans are commonly used by businesses or startups that need a lump sum for a renovation or need to purchase inventory or equipment.

If you imagine a car loan or mortgage, a business term loan is almost the same. You acquire a lump sum and invest it into something specific, then making regular repayments every two weeks to a month.

Business Lines Of Credit

Business lines of credit are useful if you don’t want full on bank loans. A business line of credit provides you temporary cash flow or relief from an unexpected expense. You can then pay off the line of credit at a later date.

The longer you wait to repay your credit line, the more interest you will end up paying as well.

CLA (Convertible Loan Agreement)

A type of debt financing that is designed for early-stage startups and provides a loan that can be converted into equity at a later date, usually at a discount, upon the occurrence of a specific event such as an equity funding round.

SBA Loans

SBA loans work like traditional bank loans and are typically run through credit unions or directly from a bank. These loans are excellent for smaller startups as they are partially guaranteed by the US

Small Business Administration, causing the average lender to be more at ease.

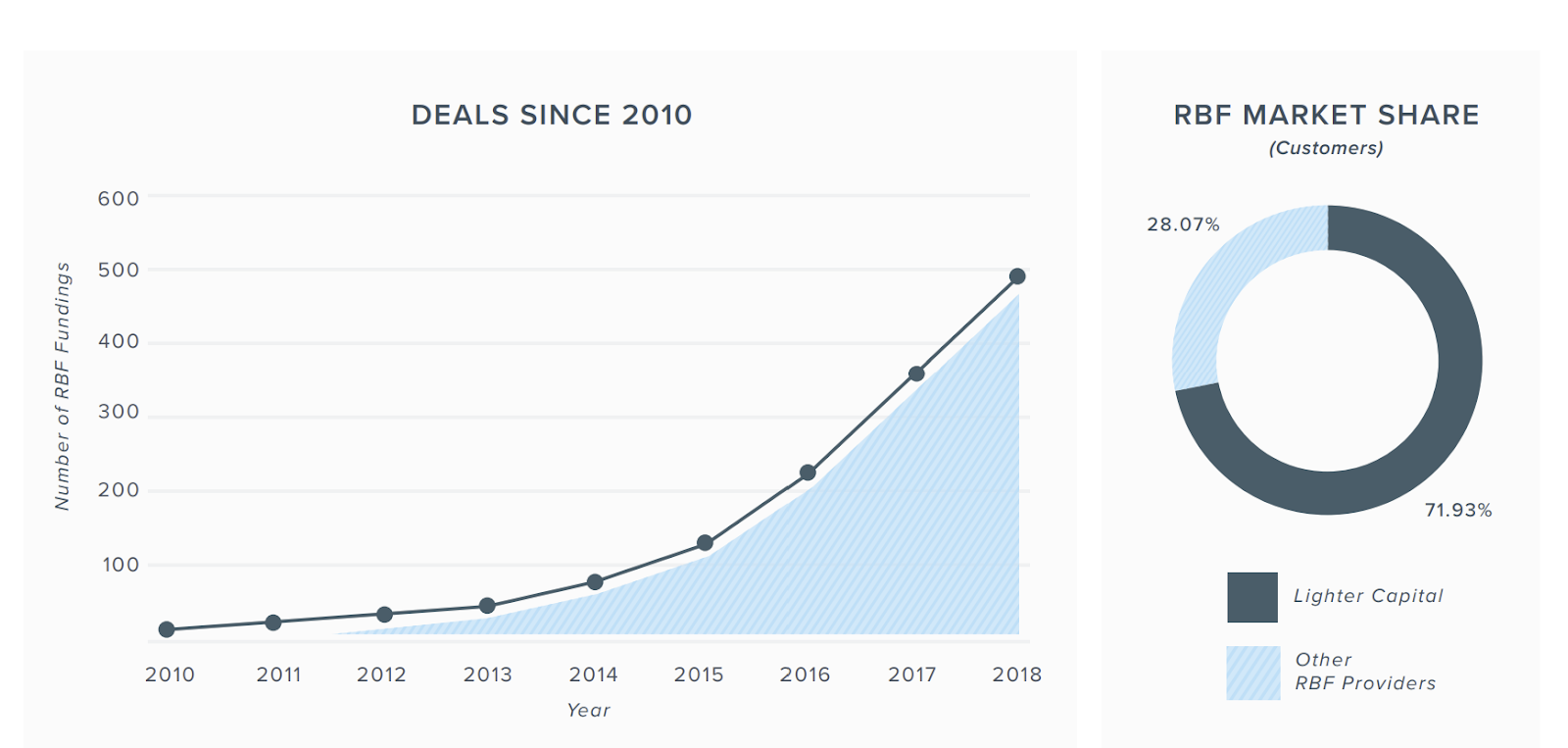

Revenue Based Financing (RBF Or Factoring)

Revenue-Based Financing (RBF) is a type of debt financing that provides startups and small businesses with working capital in exchange for a portion of their future revenue. RBF is designed for companies that have a proven business model, a growing revenue stream, and the potential for substantial future growth.

Under an RBF agreement, a lender provides a loan to the company based on its MRR volume, and in return, the company agrees to repay the loan by a set percentage of its future revenue. The loan repayment amount adjusts as the company’s revenue changes, which means that the repayment amount can be lower or higher based on the company’s performance.

RBF is a flexible financing option that can be useful for startups and small businesses that are looking for growth capital without giving up equity. It is often used as an alternative to traditional bank loans or equity financing.

Source: Lighter Capital

Business Credit Cards

A business credit card works much like a typical credit card. You won’t need the same requirements for a business credit card as you do with an individual credit card. Things like credit history and credit rating are still factors to consider, but the expected levels you are to reach for a business card are quite different.

Merchant Cash Advances

MCAs or merchant cash advances provide your startup with a lump sum to draw from which you will be expected to pay back slowly with your credit and debit sales ongoing. You will most often decide on a daily or weekly percentage of your sales that will go to the lender, meaning you won’t have to worry about repaying from your own pocket.

Pros And Cons Of Debt Financing

Depending on how much debt you can handle from a bank loan and how you wish to go about borrowing money with an interest expense answers whether debt financing will be an advantage or disadvantage to your startup’s situation. Let’s take a look at the main advantages and disadvantages for your benefit:

Pros Of Debt Financing

Tax Deductible Interest Payments

Most debt financing repayment options don’t require you to pay taxes on the interest. This applies mainly to loans from certified lenders as opposed to peer-to-peer loans.

Business Credit

Loaning money means you will start to build up positive business credit, assuming you make your payments on time. A good business credit rating makes it easier to acquire bigger and better business loans at a future date.

Retain Control Of Your Business

Debt financing allows you to maintain your business cash flow for a longer period, giving you time to work on your promotion and sales methods and improve the business’ efficiency over time.

Cons Of Debt Financing

Possible Financial Strain

If your business starts underperforming, it can be a strain to keep up with payments and monitor the business at the same time. Most lenders design the repayments around what you can afford and have measures in place for tougher times, but it is still something to consider.

Collateral Risks

Most debt financing options require some form of collateral, which means you risk losing that collateral if you end up making fewer sales and not keeping up with payments. This reason makes it more beneficial to use debt financing in late-stage startups rather than early on when you’re less sure of what your business is capable of.

FAQs

What’s The Difference Between Debt Financing And Interest Rates?

Your debt finance interest rate is dependent on how easily your company raises money, debt capital, and your firm’s capital structure. Choosing a loan with a lower interest rate is more of a risk for the lender and typically requires that you can prove a certain daily sales value. However, having a high credit rating may convince a lender to make that deal with less leverage.

High interest rates are safer for the lender, meaning they are more likely to agree to a longer term repayment period. This can help you avoid going into too much debt.

How Is Debt Financing Different From Equity Financing?

We mentioned equity financing earlier in the article. Equity financing works much like debt financing in terms of what you gain from the transaction. The difference is in how you return the money you earned.

Equity finance involves giving up a portion of your startup equity to the lender. One example would be taking a lump sum of $100,000 in exchange for 20% of your equity, meaning the supplier of the money would own 20% shares in your startup and gain that amount of your profits every day.

Unlike equity financing, debt financing doesn’t cause you to lose any of your earnings permanently. You will need to pay back the money in a shorter period than you might with equity finance, but it means the entire business assets are yours to own afterward.

Wrap Up

Debt financing isn’t a particularly complicated subject, but it is one that is often overlooked, and not always treated with the reasoning it deserves.

In other words, this isn’t something you should rush into, blindly. There are pros and cons involved with debt or equity financing which need to be well considered and analyzed carefully.

Take your time, arrive at a conclusion driven by the short and long-term implications of each option, and give your business a more stable foothold, going forward.